From Denial to $1 Million Blueprint: How Removing Inquiries Unlocks Infinite Business Funding

Every business funding hopeful knows the sinking feeling of a “denied” notification. You have the score, you have the entity, and you have the drive. Yet, the doors stay shut.

If you look at my raw Credit and Funding Log tracking an entire year’s worth of funding sequences, a fascinating—and highly educational—story emerges. It’s a journey of trial, major error, rogue brokers, and the exact “aha!” moment that changes the scaling game forever.

Here is a breakdown of what the data and artifacts tell us about the hidden mechanics of high-level business funding.

Phase 1: The Trap of Mismanaged Expectations

A lot of entrepreneurs start their funding journey applying here and applying there and not really knowing the data points that the banks are looking at. I can now truly say that I’m blessed to have found people who have researched and collected those data points either directly from the underwriters or by doing hundreds of applications and observing the results.

A standard funding playbook dictates a clear sequence: get a round of funding ($25k–$50k), pause, pay down aggressively to keep utilization low, wipe off the hard inquiries, and only then apply for the next round.

- Parenthetically here we have to make it clear that there’s also a sequence within the sequence in terms of how you hit the credit bureaus. It doesn’t make any sense to apply to three banks in a row which all hit Experian it’s best to hit one of each. For that reason any professional funder always starts their funding with Chase because they’re the most sensitive to enquiries. And because they typically pull from two bureaus and after you see what you do you can then start your 2nd application with the 3rd.

This video from Stedman Waiters clearly lays out sequencing:

I paid $5700 for his training. The thing is is he wants you to be a complete funding solution and handle everything and I don’t really feel equipped in terms of knowledge or bandwidth to do all that. I was looking for something that was where I could simply refer people and I didn’t really like the presentation pages that I had as a free affiliate that was just referring people. Not to mention that there’s no back office tracking of the people that I submit.

When impatience or management slip-ups happen—like high utilization or a late payment—the system breaks. Taking accountability for those early funding run rejections is the first step toward keeping the banks happy with you..

Phase 2: The Danger of “Wild West” Brokers

What happens when you go hunting for funding solutions on local real estate meetups or Craigslist? You often meet middlemen who lack a cohesive, long-term vision.

The data tells a chaotic story through late 2025 and early 2026:

- The Dead Ends: Groups like “Qandid” stacking consecutive rejections across major institutions like Wells Fargo, First Horizon, TD Bank, and Flagstar.

- The Personal Debt Band-Aid: Finding individual fixers who score quick wins—like two $40k personal loans through Lightstream and SoFi—which provide massive relief for credit card debt, but fail to build a corporate sequencing strategy.

- The High-Risk Operators: Rogue players who stack up personal inquiries while ignoring the damage, or worse, cross major compliance boundaries like fabricating tax returns without explicit permission just to chase a credit union approval.

When brokers operate without an exit strategy for the hard inquiries they leave behind, they leave your profile heavily restricted, resulting in strings of rejections from issuers like Capital One, Amex, and local credit unions….

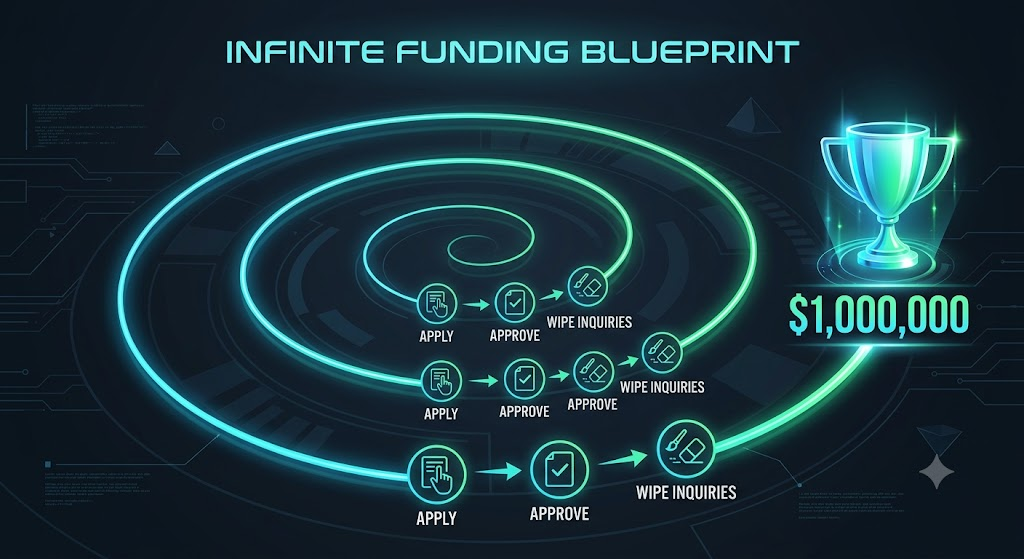

Phase 3: The “Infinite Funding Blueprint” Realization

The paradigm shift happens when you see the macro picture: Funding -> Inquiry Deletion -> More Funding.

But to unlock these and scale toward the $1 million mark, you have to solve the ultimate gatekeeper: you should never have more than 2 inquiries per bureau in the last 6 months for optimum results.

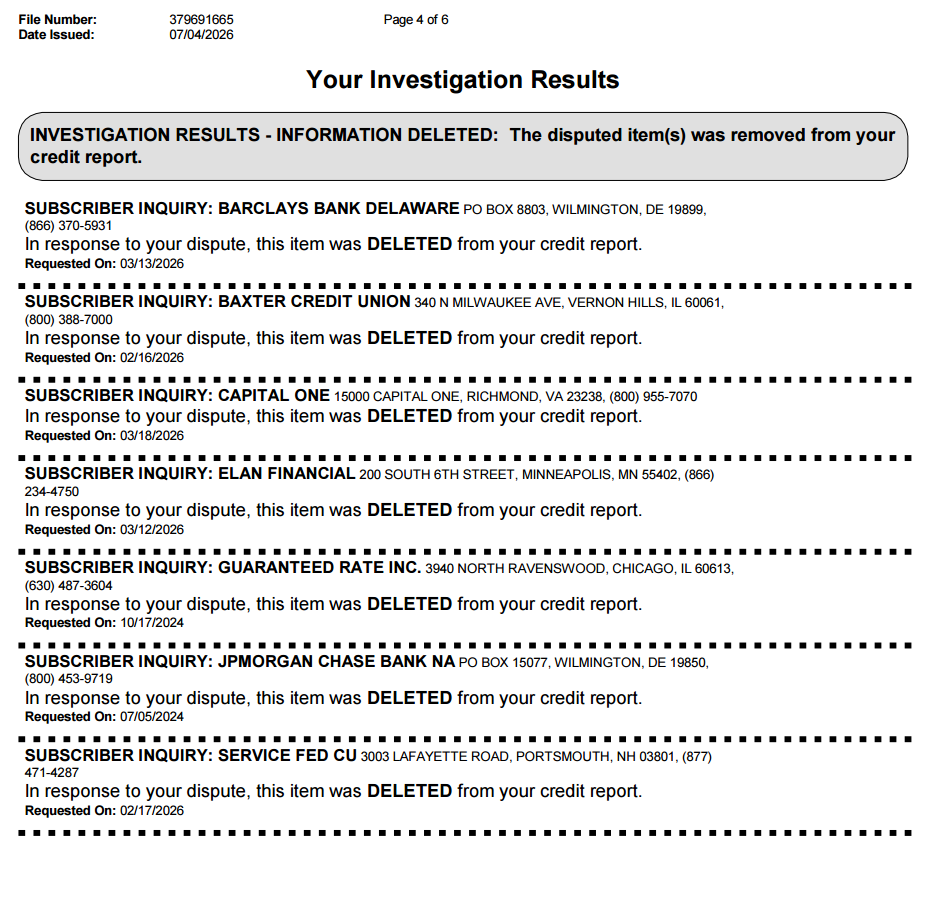

Phase 4: The Proof is in the Deletions

Hard inquiries are the friction that slows down a funding sequence. Wiping them cleanly without spending hours mailing manual dispute letters changes everything.

Recent artifacts demonstrate exactly how the bureaus handle backend automated sweeps:

1. Experian’s Rapid Response

It’s widely known that anyone can remove Experian inquiries in 2 weeks or less. I have several resources that can do that. So when my current funding and credit company came through on them They were basically batting par for the course at that point

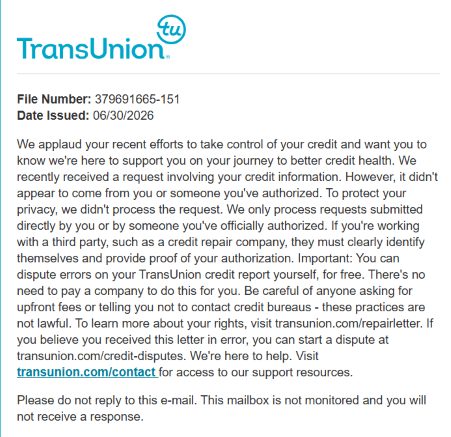

2. TransUnion’s Foot-Dragging

The road to clean credit isn’t always linear. As shown in this stall letter, TransUnion frequently issues standard, automated “roadblock” notices claiming a dispute request “didn’t appear to come from you.” This is a classic stall tactic. However,when I showed this to my funding advisor, he forwarded it to the credit team and they said: “dont worry about”. Sure enough a week or two later, they wiped the slate clean:

3. Equifax Cleanup

While fewer funders prioritize Equifax, ensuring total optimization across all three bureaus is what prepares a business profile for massive, frictionless capital stacking. The head of funding for my current credit/funding pick ( “China Credit” on Instagram) has once again earned his keep.

The Takeaway

Your credit log shouldn’t be a record of permanent defeats; it is a tactical roadmap. If your back is against the wall, remember that a string of rejections is usually just a symptom of an inquiry log that needs a heavy sweep or perhaps poor sequencing of applications. Those are your fulcrums: recent accounts, recent inquiries and sequence to apply in.

Current State

I’ve been loading up my bank accounts with cash to improve the chances of credit card approval. And I’m awaiting these Equifax inquiries to say bye-bye.

I’ve started to dance a bit with 7 figures Funding because I like the transparency of their back office and responsiveness. But they delegate credit repair to a 3rd party (and the funding advisor admitted they have gone through numerous firms for credit repair) and I wasnt impressed when I called them in stealth mode and interviewed them. I was very impressed with the tool that asks me questions and in an interactive fashion continually kept raising my score based on my answers to the questions. And the story of the founder on Instagram is quite touching because he was a fine answer for cars and notice people getting turned down for auto loans and got into credit repair to figure out how to fix them. But their answers about how quickly they could remove enquiries were less than appealing to me.

The current outfit that I’m with is a 1-stop-money-shop – they do credit repair and funding.

Other things to look out for

If a business funding output does not train you to request credit limit increases After they get you funding then they’re missing out on another 10 to $50,000 of funding.

Parting words: a repaired credit profile is not an optimized credit profile

It’s common knowledge that a person with an 820 credit score might get far less funding than someone with a 680 credit score. If the 820 credit profile is thin meaning that it hasn’t shown that the person can borrow and pay back money or if there’s a bunch of recent enquiries they could very well get denied far more than A 680 person who has a very long payment history Average account age is well over 10 years and more. So truly the steps to business funding have to do with repairing the credit profile optimizing the credit profile then getting funding and then reoptimizing it by removing inquiries ad infinitum

{kind=link}